HSA Accounts: A Tax-Advantaged Triple Threat

So . . . what if you would like to pay taxes like . . . never?

For many Americans, whether receiving health benefits through a private employer or one of the ACA exchanges, November 1 marks the start of the annual open enrollment period. It is because this date is just around the corner that I write this article now. You see, I want to expose you to the power and benefits of Health Savings Accounts (HSA).

HSAs were established in 2003, as part of the Medicare Prescription Drug, Improvement, and Modernization Act. These are tax-advantaged savings accounts available to those enrolled in a High-Deductible Health Plan (HDHP).

Photo by Hush Naidoo Jade Photography on Unsplash

HDHP’s charge lower premiums than traditional health plans, but come with higher deductibles and out-of-pocket maximums. In turn, HSAs were designed to provide tax benefits to offset these higher costs.

HSAs - The Health Angle

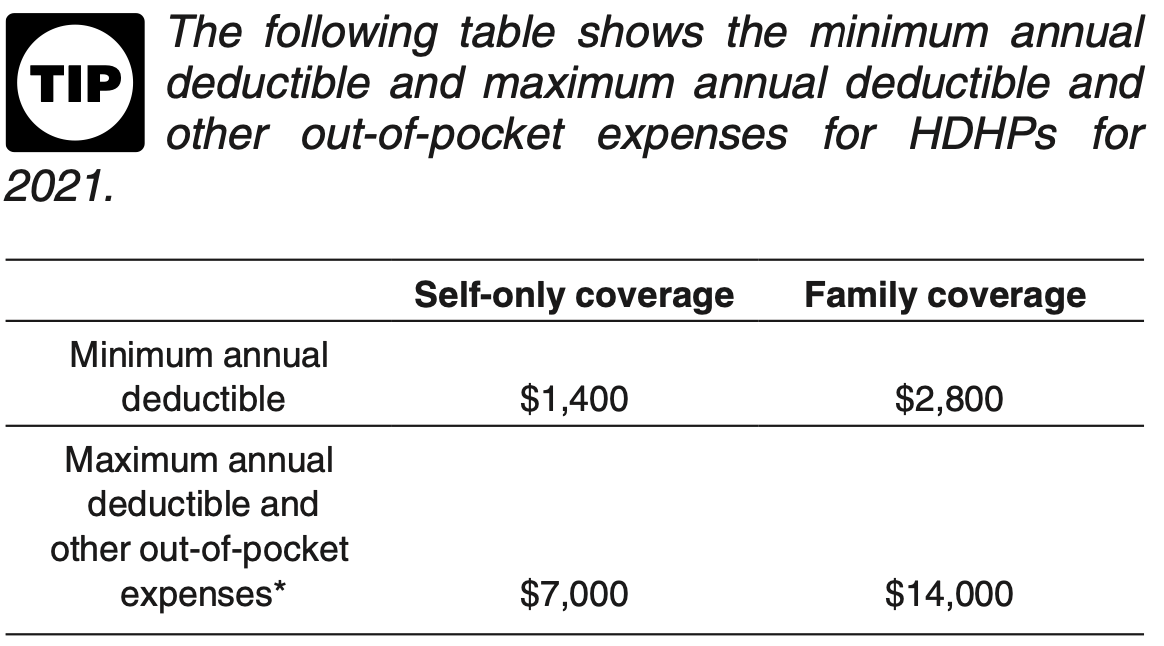

As mentioned, to qualify to open an HSA, you must enroll in an HDHP. Here, from IRS Publication 969, are the requirements for such a plan.

As seen above, the minimum annual deductible for one of these plans must be at least $1,400 for individuals and $2,800 for families and can potentially be as high as $7,000 and $14,000, respectively. Those top amounts also serve as out-of-pocket maximums, meaning insurance covers all costs past that point.

In my own case, I am enrolled in an HDHP provided by Blue Shield of California, via the Covered California ACA Plan. Both my deductible and out-of-pocket maximum are at the $14,000 limit prescribed by law for a Family plan.

If you think about it, the logic of the HSA/HDHP combination becomes clear. With the HDHP, since I am responsible for paying my own way up to the maximum deductible or out-of-pocket limit, I have a built-in incentive to shop for better health care options. In return, the HSA offers me tax benefits for doing so.

HSAs - The Tax Angle

As a primarily financial writer, however, what I really want to share with you are the tax benefits available to you with an HSA.

In my own case, it was only about 4 years ago that my employer first offered an HDHP option, so I had never really looked into HSAs prior to that. And, even in the first year the option opened up, I passed on it and went with the more traditional health plan. Why? Because under the time crunch of the open enrollment period, I didn’t feel as if I had the time to evaluate everything properly and was afraid of making a mistake. That’s why I wanted to write this article now, so hopefully you won’t find yourself in the same bind.

First off, here are the HSA contribution limits for 2021.

What, though, makes an HSA such an intriguing option, from a tax perspective? Take a look at the graphic below from a wonderful Vanguard primer on HSAs, and the answer will become readily apparent.

Let’s start with the worst option, your taxable investments. Basically, everything is taxable at your marginal tax rate. Yes, there are some minor exceptions, such as preferred rates for qualified dividends, but you get the drift. If your combined fed/state marginal tax rate is 30%, you only get to keep 70 cents out of every dollar.

IRA and 401(k) options are better. Here, your contributions are pre-tax, so you escape current taxes. And, your gains compound tax-free. However, taxes are due when the funds are withdrawn.

Roth options flip the sequence, so to speak. You pay taxes up front, on your initial contributions. From there, though, you are in great shape. Gains compound tax-free, and withdrawals are also tax-free.

Contrast all of that now with the HSA featured nicely broken out on the top section of the above graphic. How does this strike you? No. Taxes. Ever.

That’s right. Contributions to an HSA are tax-deductible up front. If paid by an employer, they are exempt from income tax. There is no requirement that they be spent in the current year, or any pre-determined length of time for that matter. As a result, if invested, all gains are tax-free. Finally, all withdrawals are tax-free.

Of course, there is a caveat. Distributions from this account may only be used for qualified medical expenses. These are defined in IRS Publication 969, as follows.

Qualified medical expenses are those expenses that would generally qualify for the medical and dental expenses deduction. These are explained in Pub. 502, Medical and Dental Expenses.

Again, this works nicely in conjunction with your HDHP. While details may vary, typically you will be responsible for paying in full the negotiated rates the insurance company receives for given medical procedures, until you reach either your deductible or out-of-pocket limit.

Example: With a traditional health plan, you may have been used to only having to fork over a $20 co-pay for a routine doctor’s visit. What that “hides” is the fact that the billed cost for that visit may be $200. But, here’s the good part, even with an HDHP. You still receive some benefit from the negotiated rates provided by your insurance provider. While the billed cost for the visit may be $200, the insurance company may have a negotiated rate of $140 that they will pay. In this example, you will be responsible to pay that negotiated amount, $140.

This is where your HSA kicks in. If you have taken advantage of the cheaper premiums offered by your HDHP by making pre-tax contributions to an HSA account, you can then withdraw, tax-free, to cover that cost.

Here, though, is an important record-keeping caveat. Be sure to keep your receipts. If ever audited by the IRS, you will need to be able to document the amounts spent on qualified medical expenses.

My Personal Scenario

You may recall that I passed on the HSA/HDHP option in late-2017, the first year it was offered by my employer, due to feeling somewhat under the gun to make a hurried decision.

To conclude this article, I am happy to share my personal journey to taking the leap a year later, in late 2018.

Replicated below is a section of the spreadsheet I used to make the decision. Take a look. Both of these options were through one of the Blue Cross/Blue Shield plans.

To that point, I had always taken the 100/50 plan. It had the highest premiums, but the lowest deductibles and potential out-of-pocket costs. Without divulging too much personal information, I will simply share that my wife and I (no kids), both in our mid-50s, have what I would describe as some level of health complications. In addition to annual physicals, these involve a small number of specialist visits, as well as one prescription for which there is no generic alternative. So, my decision was a little different than, say, perhaps an individual or couple in their 20s or 30s, in more or less perfect health and taking no medications.

The first factor I took note of was that, in taking this plunge, I would immediately start saving $308 per month in premiums (deducted twice monthly from my paycheck), or roughly $3,700 per year. In return, I accepted $2,400 in additional expense risk before hitting my deductible. Interestingly, take a look at the bottom line. Overall, my out-of-pocket maximum only jumped by $1,600.

My ultimate decision was to go for it. Simultaneously, I set up an automatic payroll deduction to fund the HSA account at the full limit allowed by law. The savings on premiums took care of about half of it, with an additional voluntary deduction covering the rest.

In the first year this was active, 2019, we had a slightly higher than average amount of medical expenses. As a result, we just about broke even on the deal. Our HSA ended the year with a balance of roughly $4,000, about the difference between the premium savings and the higher contributions to the HSA.

In 2020, we had a better year, with less medical expenses, and our HSA ended the year with roughly a $9,000 balance. As I write this in October, 2021, we sit with roughly $12,000 in the account.

Final Thoughts

Sharp readers may have caught the fact that, starting November 1 of this year, my HDHP will be through the Covered California program, and that my deductibles and out-of-pocket limits are higher.

Why is that? It is because, as of October 31, I am retiring! In my particular situation, I was able to get a better deal through Covered California than the COBRA options available through my employer.

Interestingly, this opens up some entirely new and different possibilities for me to explore.

I hope to share some of these in a future article, or articles.

If you have any questions, please feel free to . . .

If you are not already a subscriber, simply click the button below to join the fun.

Finally, if you have friends, coworkers, neighbors, or anyone else you think might find this helpful, click on the button below to share this post.

Thanks for honoring me with your time by reading my article! I hope to see you next time.