Family Offices - Cautious At Present, Optimistic For The Future

In which I seek to benefit from the best thinking of professionals who manage money for the very wealthy.

“This year we are neutral everything. Even with equity we are not underweight or overweight. We are not taking big bets on anything.”

CIO of a Singapore-based Family Office

This past June 12, I wrote an article entitled Rethinking 60/40 - Your Best Portfolio Right Now Might Be 30/30/40. At the time I wrote that article, I had already begun my review of Global Family Office Report 2023, a recently-released document from UBS. As you consider this article, you will likely see the connection between the two.

Before we go any further, for any who may be unfamiliar with the term, a family office is a private wealth management advisory firm that serves an ultra-high net worth individual or family. In addition to financial planning and investment management, many family offices offer budgeting, insurance, charitable giving, wealth transfer planning, tax services, and more.

This report is the 4th annual such survey undertaken by UBS. For 2023, 230 family offices participated in the survey. The average net worth of participating families is $2.2 billion. On average, their family offices manage $0.9 billion.

In this article, I will summarize key takeaways from the report, as well as drill down into a few of the details.

Summary of Key Takeaways

The 2023 report begins by noting that it comes at a defining moment in time, with the end of the era of low and even negative nominal interest rates and the ample liquidity provided following the global financial crisis. As a result, family offices are planning the biggest modifications in strategic asset allocation in several years.

Here are some high-level takeaways from the report:

Over the next 5 years, family offices are looking to add developed-market fixed income holdings over the years to come and are already diversifying portfolios through high-quality-short-duration fixed income.

Family offices are planning to raise holdings in emerging market equities, following a perceived peak in the US dollar and the reopening of the Chinese economy.

Overall, and while this varies somewhat by region, geopolitics has replaced inflation as the top concern for family offices. In the US, recession remains the top concern while in Europe and the Asia-Pacific region, geopolitics tends to be the foremost concern.

Family offices are increasing their allocations in regions that have been less in favor for the past few years. While they still have roughly half their assets in North America, over a quarter are planning increased allocations in Western Europe and the Asia-Pacific region.

When it comes to alternative asset classes, such as private equity secondaries, family offices intend to use their investment flexibility as a competitive advantage. To the extent that other limited partners are forced to seek liquidity due to portfolio rebalancing or forced selling, they would hope to step into the void and overallocate at bargain prices.

Broadly speaking, the family offices interviewed for the 2023 report were cautious about current markets in the face of the uncertain growth outlook in developed economies, as well as tighter lending conditions and heightened geopolitical tension. This is reflected in the featured quote with which I opened this article, as well as the one directly below.

“Last year, we probably allocated $30 million to $40 million of new capital but probably liquidated $180 million. Right now, we probably have about a third of our capital in cash. If I look through to the managers we invest with (who are also heavily in cash), we are probably 50% in cash.”

CIO of a US-based Family Office

Current Asset Allocations

In terms of current asset allocation, the below graphic offers a comprehensive overview.

It is interesting to note the top-level breakdown. At this level of wealth, some 55% is invested in traditional asset classes (e.g. equities, fixed income, cash) with 45% being allocated to alternative asset classes (e.g. private equity, real estate, hedge funds).

Even here, though, the value of diversification becomes clearly evident. For example, in the case of both equities and fixed income, global diversification is evident, including balanced investment in emerging markets.

Looking To The Future

Looking beyond 2023, over the next five years family offices anticipate making more changes to their strategic asset allocation. After cutting back on bond holdings over the past three years, the biggest turnaround is in developed-market fixed income, where 38% of the family offices surveyed plan on a significant or moderate increase in allocations.

They also foresee greater allocations to risk assets in general, with 44% planning increases in developed market equities and 34% in emerging market equities. Looking forward five years, 30% of family offices intend to shrink cash allocations.

One area of caution relates to real estate. Family offices cautiously planned to cut allocations in 2023. At the same time, over the next 5 years some 33% foresee moving to higher allocations. This fits a picture of interest rates remaining high in 2023, with related softness in real estate prices, before easier money and lower valuations start to support this asset class once again.

In terms of asset classes, here is how family offices anticipate modifying their allocations over the next 5 years.

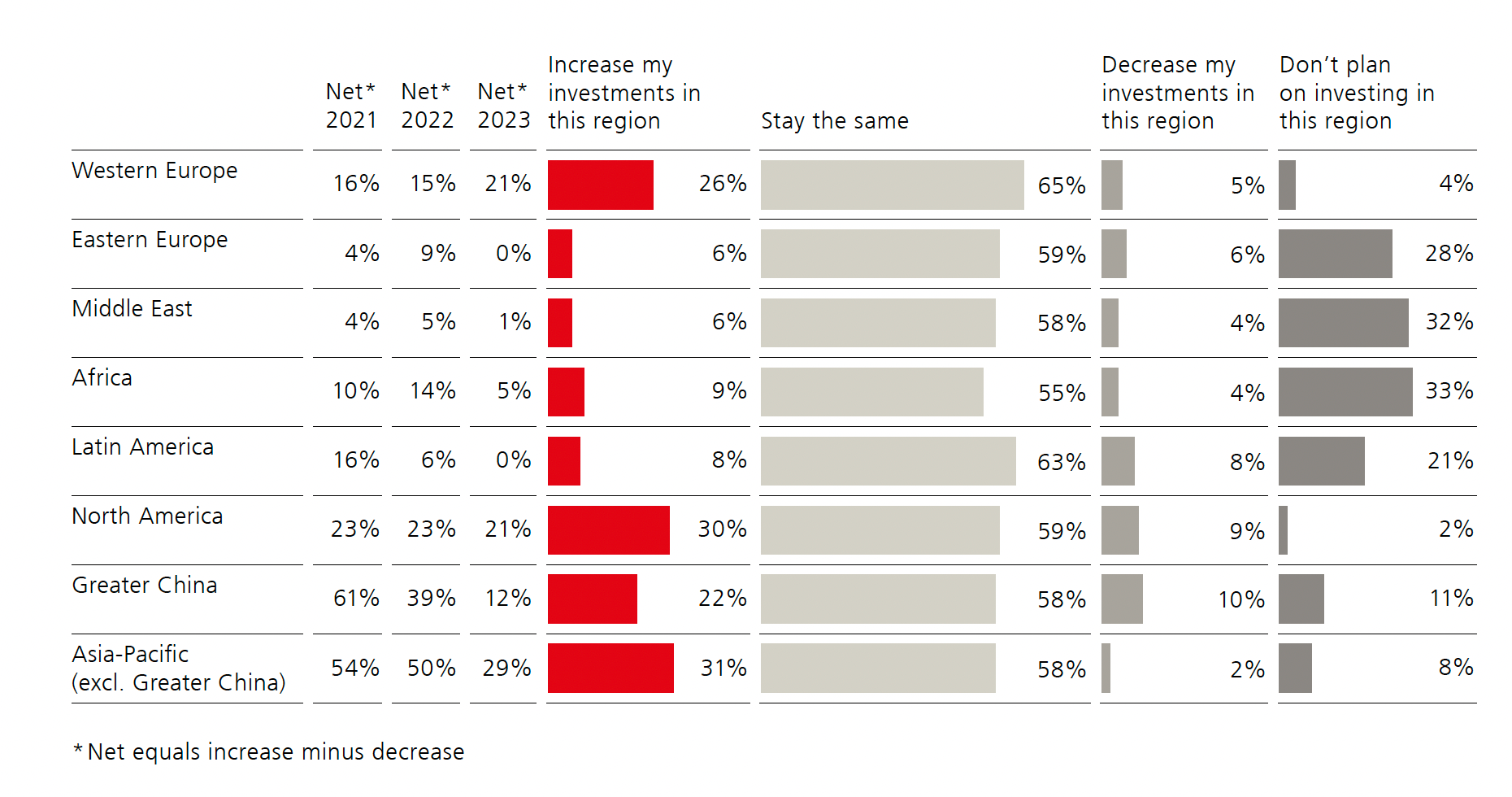

With respect to geography, at present North America, at 48%, and Western Europe, at 30%, continue to be the two largest areas of asset concentration. Looking forward, there is a broad-based increase in interest in Western Europe, with some 26% of family offices intending to increase allocations over the next 5 years. Moving to the Asia-Pacific region, some 31% anticipate raising holdings in areas outside Greater China. At 22%, a slightly lower percentage anticipate raising allocations inside Greater China.

In terms of geography, here is how family offices anticipate modifying their allocations over the next 5 years.

To conclude this section, while family offices tend to be cautious about the present, as featured in the two earlier quotes I specifically called out, they are just as excited about the future. Here’s a quote representing the other side of the coin, so to speak.

“We are quite excited about this environment, as we think this kind of environment is a lot more attractive. For instance, we invested in 2020 because we saw opportunities. We keep cash for situations like these. We hope over the next few years to reduce our cash balance.”

CIO of a Swiss family office

Other Takeaways

Here are just a few other key takeaways from the report.

Digital Transformation

Digital transformation is the investment theme that resonates most with family offices. Here is a nice graphic featuring the Top 6 overall investment themes.

Private Equity & Debt

Interestingly, while family offices have reduced allocations to direct private equity, they appear to be ready to raise holdings in private equity funds, private debt and infrastructure. Some 66% of family offices appear to hold the belief that illiquid asset classes offer the potential for superior returns. Here is one related quote.

“We are discussing whether the equity boom of the last 15 years where money was free has been followed by an inflection point that indicates a different environment. That’s leading to conversations about increasing allocations to quality private credit.”

CEO of a UK-based Family Office

Real Estate

As featured earlier in the article, while family offices tend to be cautious with respect to real estate at the present time, a substantial percent plan to increase allocations over the next 5 years.

However, the outlook varies by region. European (including Swiss), Latin American and US family offices foresee increasing allocations, while fewer Asia-Pacific investors see themselves doing so.

Finally, in a sector where location is everything, family offices prefer to stay close to home. Of the total, roughly 62% of the total is domestic, with the balance of 38% being allocated to international real estate.

The Report’s Effect On My Portfolio

In my most recent post, I shared my personal portfolio and asset location update for Q2 2023.

While, as I frankly admit, I have been surprised at the strength of the market rally thus far in 2023 and my portfolio might be judged to have underperformed, this report served to help me gain greater comfort with my situation and decisions.

As a recent retiree, my focus is first and foremost on capital preservation. At the present time, then, my cash level is higher than it will likely remain over the longer term. Understanding that a substantial percentage of these family offices are structuring themselves similarly was helpful to me. In my personal case, I am hoping to have opportunities to put my rather substantial cash holdings to work at better prices.

I hope this summary has given you much to think about with respect to your personal situation. While this is different for each of us, hopefully the principles used by those who invest on behalf of the very wealthy can trickle their way down to helping the rest of us make solid decisions.

Excellent writeup. You really add a lot of value to all of us. Thanks.